5 key differences of SET ESG Ratings and FTSE Russell ESG Scores

Why FTSE Russell Matters for Thai Companies

ESG is no longer just about “responsibility”—it has evolved into an “investment standard” that drives global investor decision-making. The Stock Exchange of Thailand’s transition from SET ESG Ratings to FTSE Russell ESG Scores represents far more than a procedural change. It’s a pivotal shift that every listed company must understand and prepare for strategically.

FTSE Russell stands as a globally recognized ESG index and risk assessment provider, operating across over 80 countries worldwide and evaluating more than 85,000 companies throughout Europe, the Americas, and Asia. Its core strength lies in relying exclusively on publicly disclosed information, ensuring transparency, comparability, and verifiable assessment standards that meet international benchmarks.

To help Thai listed companies navigate this transition effectively and leverage this opportunity to elevate their organizational sustainability, this article examines the 5 fundamental differences between SET ESG Ratings and FTSE Russell ESG Scores. We’ll explore the transition roadmap you need to understand and provide systematic preparation strategies for your organization.

The 5 key differences Thai ESG Ratings/Scores

1. Scoring Systems and Performance Disclosure

One of the most significant distinctions between SET ESG Ratings and FTSE Russell ESG Scores lies in their “scoring methodology” and “public disclosure” of results—a paradigm shift that fundamentally impacts corporate reputation, transparency, and investor confidence.

Under SET ESG Ratings, companies receive tier-based ratings (BBB, A, AA, or AAA) only when they meet minimum qualifying thresholds. Beyond achieving scores above 50% across each dimension (Environmental, Social, Governance), companies must satisfy additional requirements such as maintaining a CGR rating of at least 3 stars and demonstrating no negative governance issues during the assessment period. Companies failing to meet these criteria receive no public rating disclosure whatsoever.

FTSE Russell ESG Scores takes the opposite approach, implementing unconditional disclosure of all company scores using a decimal-based system ranging from 0.0 to 5.0. Regardless of performance level, all scores will be publicly announced starting in 2026, providing open access to investors and the general public.

While detailed insights such as thematic scores, dimensional breakdowns, or individual indicator performance remain accessible only within FTSE Russell’s proprietary system using company-specific access codes, the overall score—representing your organization’s “ESG identity” on the global stage—becomes universally visible. Whether you achieve a 4.8 or 0.9, the result is transparent to all stakeholders.

This transparency extends beyond mere openness to directly impact corporate “credibility.” Low scores without adequate explanation or appropriate disclosure may lead investors to conclude that the organization lacks genuine ESG commitment or systematic sustainability management practices.

This difference transcends scoring methodology—it represents a fundamental shift from “seeking assessment” to “communicating transparency” continuously through verifiable, publicly disclosed information.

In an era of heightened investor focus on ESG factors, companies that strategically manage their disclosure practices will not only achieve scores reflecting their true potential but also earn sustainable “stakeholder confidence.”

Summary

SET ESG Ratings

- Scores only companies that “meet qualifying thresholds”

- Announces results in tier format: BBB, A, AA, AAA

FTSE Russell ESG Scores

- Scores all companies regardless of performance level

- Uses decimal scoring format: 0.0–5.0

- Publicly announces overall scores starting in 2026

- Detailed insights (thematic scores, dimensions, indicators) accessible only through company-specific system access

The Advantage

FTSE Russell operates on principles of “transparency and equality”—every company has the opportunity to communicate ESG progress, not just those meeting minimum thresholds.

2. ESG Data Collection Methodology

Another game-changing distinction lies in the approach to ESG data collection. SET ESG Ratings requires companies to voluntarily register and complete comprehensive questionnaires with extensive supporting documentation from both public sources and internal records for Stock Exchange evaluation.

FTSE Russell ESG Scores eliminates questionnaires entirely, instead evaluating companies based solely on “publicly disclosed information”—sustainability reports, annual reports, Form 56-1 One Reports, and corporate websites. No internal documentation receives consideration.

This philosophy reflects international capital market principles emphasizing the ability to “communicate sustainability” directly, clearly, and accessibly. Companies capable of systematically disclosing ESG information can confidently navigate assessments without dedicating time and resources to hundreds of questionnaire responses.

Simultaneously, this signals that ESG disclosure should not be limited to assessment seasons but should represent “continuous public transparency”—robust, evidence-backed, and consistently verifiable information.

Summary

SET ESG Ratings

- Companies must register and complete assessment forms

- Requires internal documentation such as undisclosed policies and reports

FTSE Russell ESG Scores

- No registration or form completion required—all listed companies assessed automatically

- Uses exclusively publicly disclosed information:

- Sustainability Reports

- Annual Reports

- Form 56-1 One Reports

- Official corporate websites

The Advantage

Companies avoid duplicative work while establishing “comprehensive disclosure systems” that are accurate, complete, and easily accessible—benefiting investors and all stakeholders alike.

3. Review Process and Supplementary Information

FTSE Russell recognizes that assessments based solely on public disclosure may contain gaps, therefore designing a process enabling companies to review and provide additional information before final results are announced. Companies receive email notifications from FTSE4GOOD approximately September through October each year to access the FTSE Russell Platform and review their preliminary results.

Within this system, companies can provide commentary, submit additional reference documents, or clarify information not yet reflected in public sources. Organizations have approximately one full month to complete this process—a critically important window of opportunity. Once the deadline passes, FTSE Russell closes the system, accepts no additional information, and proceeds to finalize scores officially, announcing results in December of the same year.

This period represents a golden opportunity for companies to provide context, supplement missing information, or correct misunderstandings before final scores are transparently published to global investors and stakeholders. Importantly, these scores remain unchanged until the following year’s assessment cycle.

Companies missing this window—whether due to outdated contact information preventing notification receipt or lack of system response—must accept scores based solely on available information. In cases of low scores, this can immediately impact reputation and investor confidence on the international stage.

FTSE Russell provides companies the opportunity to

- Review preliminary results and provide feedback within the system

- Timeframe: September–October annually

- Duration: Approximately one month

- Method: Email notifications sent to designated company contacts

Companies can use this period to:

- Verify information accuracy

- Provide supplementary information or correct discrepancies

- Update contact details to avoid missing notifications

Upon deadline expiration, FTSE Russell finalizes and announces scores in December.

4. Business Grouping and Industry Classification Systems

An accurate ESG assessment cannot apply uniform criteria across all businesses, as risks and material issues vary distinctly by industry. Business classification represents another critical difference between SET ESG Ratings and FTSE Russell ESG Scores.

Business Grouping and Industry Classification of SET ESG Ratings

It employs the Stock Exchange of Thailand’s classification structure, dividing companies into 8 major industry groups:

- Agribusiness & Food

- Consumer Products

- Financials

- Industrials

- Property & Construction

- Resources

- Services

- Technology

Each group subdivides into 28 business sectors for assessment and comparison of similar companies—such as banking, energy, food & beverage, communications, etc. While suitable for Thai capital market management, this system has limitations in granularity and alignment with global ESG standards. Despite effectively reflecting the Thai market overview, it cannot achieve the depth of segmentation or international benchmarking required for sophisticated analysis.

Business Grouping and Industry Classification of FTSE Russell ESG Scores

It utilizes the ICB (Industry Classification Benchmark)—a globally recognized industry classification system used by investors and stock exchanges across over 80 countries, enabling accurate and fair cross-sector, cross-border company comparisons.

ICB divides industries into 11 primary groups:

- Oil, Gas and Coal – Traditional energy businesses including oil, natural gas, coal

- Basic Materials – Raw materials and mining including metals, chemicals, plastics, paper

- Industrials – Machinery, heavy industry, engineering, general manufacturing

- Consumer Discretionary – Non-essential goods and services including automotive, apparel, furniture, entertainment

- Consumer Staples – Basic consumer goods including food, beverages, pharmaceuticals, essential retail

- Healthcare – Hospitals, pharmaceuticals, biotechnology, healthcare services

- Financials – Banking, insurance, funds, and various financial services

- Real Estate – Property development, asset management for residential, commercial, or industrial properties

- Technology – Software, hardware, electronics, telecommunications, IT services

- Telecommunications – Telephone networks, internet, satellite, and other communication services

- Utilities – Public utilities including electricity, water, gas, and renewable energy

ICB extends beyond primary industry groups, subdividing into 20 Supersectors, 45 Sectors, and ultimately 173 Subsectors at the most granular level. This enables FTSE Russell assessments to identify ESG issues material to each specific business type with precision.

For example, a property development company operating in Thailand might be classified under “Real Estate Development,” which has entirely different indicators from “Real Estate Investment Trusts (REITs)” or “Construction & Engineering,” despite all falling under the broader real estate category.

Furthermore, FTSE Russell considers the operational country context. Companies based in developing countries may need greater emphasis on human rights or anti-corruption measures rather than carbon issues in certain cases. The system analyzes “materiality levels” for each ESG theme, then weights indicators appropriately for that specific business. This represents “Context-Based ESG Scoring”—emerging as the new global standard.

Summary

SET ESG Ratings

- Uses Thai Stock Exchange criteria

- Divides into 8 industry groups / 28 business sectors

FTSE Russell ESG Scores

- Uses ICB – Industry Classification Benchmark

- International standard used across 80+ countries

- Divides into 11 primary industry groups with detailed segmentation to 173 subsectors

- Considers “primary revenue sources” identified in financial statements and One Reports

- Multi-business companies may span multiple subsectors

- Considers “operational country context” concurrently

Strength

FTSE Russell assesses based on “actual business risks” and country context, delivering accurate and internationally relevant ESG profiles.

5. Indicator Quantity and Complexity Levels

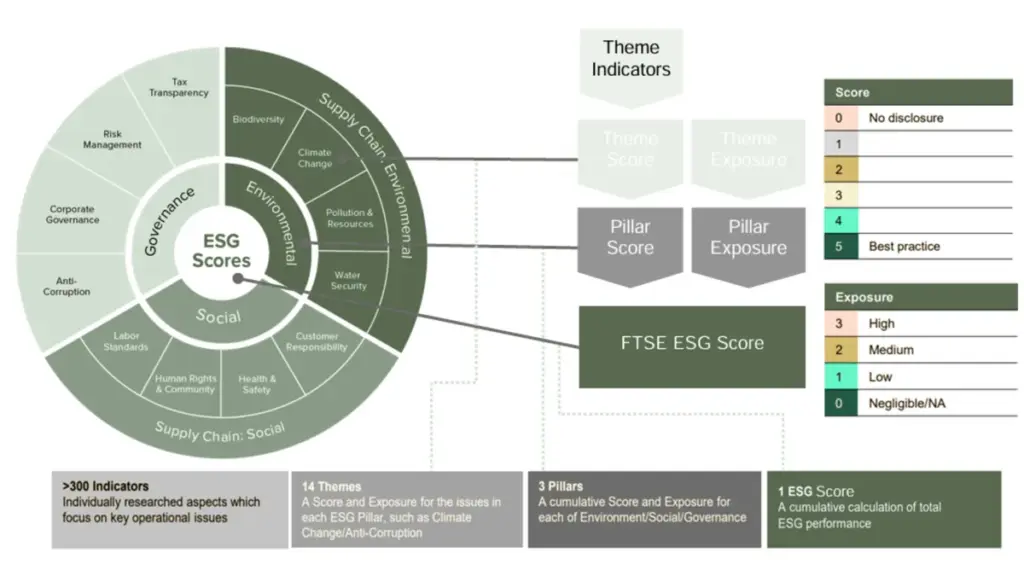

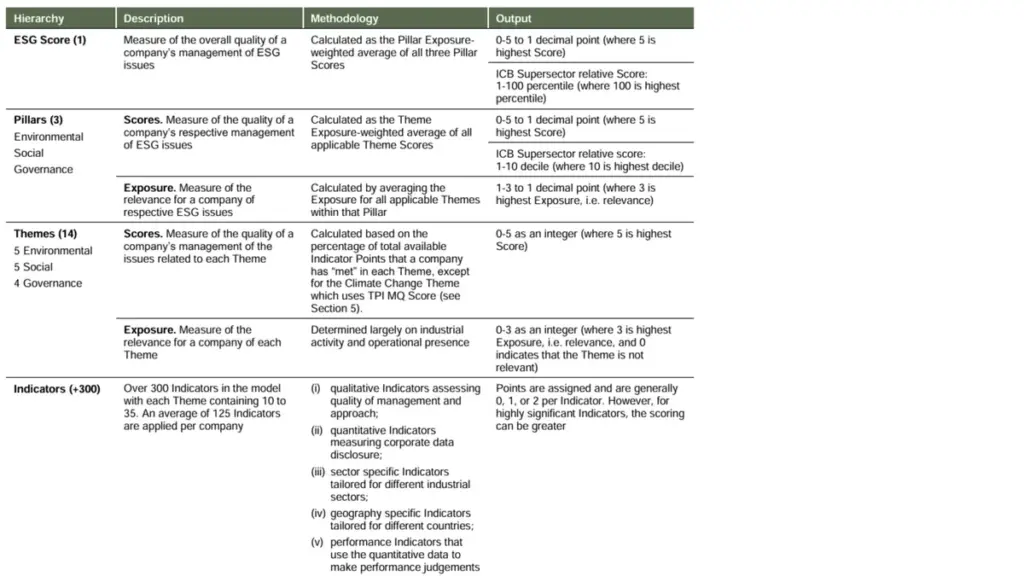

While both SET ESG Ratings and FTSE Russell ESG Scores measure from similar core dimensions—Environmental (E), Social (S), and Governance (G)—the clear distinction lies in the depth, specificity, and structural design of FTSE Russell’s indicator framework.

SET ESG Ratings employs approximately 140-150 indicators, predominantly general metrics applied universally across all industries, with only minimal adjustments for specific business characteristics.

FTSE Russell ESG Scores utilizes a more comprehensive and flexible indicator set, comprising over 300 indicators divided into two categories:

Universal indicators representing approximately 56%

Sector- and Country-specific indicators comprise the remaining 44%, which vary according to industry characteristics and the operational context of each country.

Each company is not assessed against all 300+ indicators simultaneously, but rather evaluated on what is “genuinely material,” averaging approximately 125 indicators per company. This reduces reporting burden while enabling scores to more precisely reflect organizational capabilities.

All FTSE Russell ESG Scores indicators are categorized under 14 ESG Themes linked to systematic global ESG risks, organized across three core dimensions:

Environmental

- Biodiversity

- Climate Change

- Pollution and Resources

- Water Security

- Supply Chain (Environment)

Social

6. Human Rights and Community

7. Labor Standards

8. Health and Safety

9. Customer Responsibility

Governance

10. Risk Management

11. Tax Transparency

12. Anti-Corruption

13. Corporate Governance

14. Supply Chain (Social)

The distinctive feature of FTSE Russell’s system lies in risk materiality assessment for each theme across industries, categorized into four levels:

- High (Very high risk)

- Medium (Moderate risk)

- Low (Low risk)

- Not Relevant (Not applicable)

When any theme receives a “Not Relevant” (N/A) assessment for a specific business, the company will not be evaluated on that theme, and it will have zero impact on overall ESG score calculations.

For example, if a company operates in digital services, “Water Security” might be classified as Not Relevant due to minimal water usage in operations. Conversely, for mining or agricultural businesses, this theme might receive a High classification, requiring serious management and disclosure commitments.

Additionally, certain indicators maintain heightened intensity requirements, such as three-year historical data disclosure, external verification, or demonstrable impact measurement rather than mere policy statements or commitments.

This comprehensive approach means FTSE Russell ESG Scores evaluate not just “what organizations have” but rather “how organizations manage risk and create transparency” in matters most material to their specific context.

Summary

SET ESG Ratings

- Approximately 140-150 indicators

- Predominantly general metrics

FTSE Russell ESG Scores

- Over 300 indicators

- Divided into:

- 56% universal indicators

- 44% specific indicators (industry + country-specific)

- Certain indicators maintain high intensity requirements:

- Three-year historical data disclosure

- External verification requirements

Recommendation

Companies should systematically study FTSE indicators to strategically plan comprehensive disclosure aligned with their specific context.

Timeline for FTSE Russell ESG Scores Transition

| Year | Development |

| 2024 | Leading listed companies begin pilot FTSE Russell assessments |

| 2025 | Companies may “voluntarily” request assessments |

| 2026 | FTSE Russell ESG Scores fully operational, officially replacing SET ESG Ratings |

Preparation Strategies for FTSE Russell ESG Scores

1. Develop Transparent ESG Data Architecture

As Thailand’s ESG assessment system transitions from questionnaire-based evaluation to comprehensive public disclosure assessment, companies preparing for FTSE Russell ESG Scores must establish not only clear ESG policies but also “disclosure systems” that are transparent, systematic, and accessible beyond previous requirements.

Preparation extends beyond content to encompass processes, mindset, and continuity of information that organizations choose to communicate publicly through published documents, website-hosted reports, and internal systems supporting consistent disclosure practices.

2. Enhance Website Disclosure Systems

Corporate websites, typically the first point of reference, require structured ESG or IR (Investor Relations) menu organization with current information and comprehensive linkage to critical documents such as Sustainability Reports, ESG Policies, GHG Emissions data, and organizational values. This prevents assessor confusion or misinterpretation from fragmented information.

3. Verify Three-Year Historical Data

FTSE Russell considers three-year historical data across multiple indicators, particularly for trend analysis such as carbon reduction or female executive representation. Companies should ensure quantitative evidence (KPIs and performance data) is maintained consistently and consider external verification (auditor or verifier certification) for certain data points to enhance disclosure credibility.

4. Update Company Contact Information

This seemingly minor detail often causes organizations to miss critical opportunities, especially approaching annual assessment periods. Organizations not receiving FTSE4GOOD email notifications during September-October will forfeit opportunities to review preliminary results or submit additional system information, potentially resulting in December score announcements that fail to reflect current company data.

The Transition as Strategic Opportunity (Not to Be Overlooked)

FTSE Russell ESG Scores represents more than a “new assessment system”—it’s a powerful opportunity to elevate Thai organizations’ internal management capabilities and genuinely open doors to the global ESG stage.

Many perceive ESG disclosure as burdensome—filled with reports, indicator tables, and management obligations. In reality, organizations beginning with proper system establishment from the outset discover it’s not only manageable but becomes a process enabling profound organizational self-examination in previously unconsidered dimensions.

Data previously scattered across departments, explanations once limited to “internal use,” and problems whose “root causes remained unknown” gradually emerge clearly as you systematize, create disclosure frameworks, and communicate authentically.

This represents an organizational “transformation” period—not for assessment compliance but for identifying inefficiencies, financial leakages, or hidden risks, and areas deserving reinforcement because they create long-term business and sustainability value.

Early-adopting companies gain advantages beyond scoring—they achieve “self-awareness and understanding.” When you know your global positioning, you advance with greater confidence than others.

In the ESG landscape, transparency isn’t a burden but a tool for building credibility and strategic advantage, plus organizational self-understanding—all beginning with strategic and intentional “disclosure.”