The ESG Reporting Season Starts Now. Why Organisations Should Not Wait Until Year End

With only half a year left, is it time to start preparing ESG reporting data?

Mid-year is often the time when many organisations have only just begun to catch their breath after the annual reporting and sustainability reporting season. For many companies, the annual report and sustainability report were only recently finalised, submitted, and published during the first quarter.

But for teams responsible for ESG data or Sustainability Report development, the important question is this: should we wait until year-end before starting to collect ESG data again?

The answer is no.

ESG reporting today is no longer simply about compiling sustainability-related activities and presenting them in a complete report. It is increasingly moving toward disclosure that is more closely connected to business strategy, risk management, operational performance, and financial information, especially under the direction of the IFRS Sustainability Disclosure Standards, which comprise IFRS S1 and IFRS S2 developed by the International Sustainability Standards Board, or ISSB.

IFRS S1 requires organisations to disclose information about sustainability-related risks and opportunities that could affect the entity’s cash flows, access to finance, or cost of capital over the short, medium, and long term. Meanwhile, IFRS S2 focuses on climate-related disclosures, covering governance, strategy, risk management, as well as metrics and targets.

In Thailand, the Securities and Exchange Commission has communicated its direction to enhance sustainability-related disclosures by issuers and listed companies in alignment with the ISSB Standards. In the initial phase, the focus will be placed on climate-related information, or climate-first reporting, together with the disclosure of greenhouse gas emissions covering Scope 1 and Scope 2, as well as a more standardised and credible assurance process.

This is why the second half of the year is not too early to start preparing ESG data. In fact, it is the right time to put the data system in place before the reporting season returns.

Common challenges when ESG reporting starts too late

Many organisations are familiar with the same recurring situation when the reporting period begins. ESG data may still be incomplete. Data sources may not be clearly identified. Supporting evidence may not align with the disclosed figures. Data from subsidiaries, suppliers, and internal departments may also arrive in different formats, requiring significant time to organise, validate, and reconcile.

These issues may once have been seen as a normal part of the reporting process. However, under increasingly rigorous disclosure standards, “good enough” data may no longer be enough.

Today, a credible ESG report needs to be able to answer several key questions. Where does the data come from? Who owns the data? How was it calculated? Is there supporting evidence? How does it connect to the organisation’s risks and opportunities? And can the data be traced and reviewed retrospectively?

What should organisations start preparing in the second half of the year?

The first step is to review the ESG data required for this year’s report. This should include data disclosed in previous years, data required by the reporting standards currently used by the organisation, and any new information that may need to be prepared in response to the direction of ISSB, IFRS S1, and IFRS S2.

Organisations should then clearly identify the owner of each data point. This helps clarify which department is responsible for environmental, social, governance, human resources, supply chain, risk, finance, and operational data, and who is accountable for collecting, reviewing, and confirming that data.

An ESG data collection plan or data calendar should also be developed for each relevant department. This should define the reporting timeline, data format, collection method, and required supporting evidence from the beginning of the process. Doing so can help reduce inconsistencies in data formats and prevent the Sustainability team from spending the end of the year correcting data point by point.

Another area that should begin immediately is the review of supporting evidence for ESG disclosures, particularly for key quantitative indicators such as energy consumption, water use, waste, occupational accidents, employee training, grievances, human rights, supplier assessments, and greenhouse gas emissions.

For climate-related data, organisations should prepare Scope 1 and Scope 2 information with greater readiness, including organisational boundaries, calculation methodologies, emission factors, supporting documents, and assurance processes. At the same time, organisations should begin developing a system for Scope 3 data, which relates to the value chain and supplier information, as this type of data requires time to request, collect, verify, and align across relevant parties.

Finally, internal review should take place before year-end, not only when the report is close to completion. This process should involve Sustainability, Finance, Risk, Operations, Procurement, Human Resources, Investor Relations, and senior management. ESG data should not be treated merely as information for reporting, but as information that reflects how the organisation is being managed in practice.

ESG reporting should not be the responsibility of the Sustainability team alone

The key to ESG reporting in this new era is shifting from “report production” to the development of an organisational data system.

Sustainability-related information involves many functions, from corporate strategy, risk management, costs, procurement, resource use, employee management, supplier management, and corporate governance to potential financial implications in the future.

The IFRS Sustainability Disclosure Standards emphasise information that is useful to investors and users of general purpose financial reports. The focus is on disclosures that help users understand how sustainability-related risks and opportunities may affect the prospects of the organisation. Therefore, organisations that want to strengthen their ESG reporting should begin by strengthening their internal data system, rather than waiting until the reporting period to start collecting information.

A good ESG report is not the most beautiful report, but the most credible one

As ESG standards become more rigorous, a good report is not necessarily the one with the most beautiful design or the highest number of pages. It is the report that is supported by reliable data, clearly traceable sources, reviewable evidence, and a genuine reflection of how the organisation is systematically driving sustainability.

When organisations start preparing data in the second half of the year, the outcome is not only a report that can be completed on time. It is also a more structured working process, stronger collaboration across departments, and ESG data that is ready for reporting, assessment, and long-term strategic decision-making.

Because good ESG reporting should not begin when everything becomes urgent. It should begin while the organisation still has enough time to build a data system that is accurate, complete, and credible.

How many disclosure channels are needed for an ESG report to achieve a good score?

How to prepare one ESG dataset for different disclosure channels, effectively.

Many organisations spend an entire year developing ESG policies, collecting performance data, and preparing comprehensive sustainability reports. Yet, when ESG assessment results are released, many are surprised to find that their scores do not fully reflect the work they have actually undertaken.

One of the questions we are most frequently asked is:

“Is having an ESG Report alone enough?”

The answer is not necessarily.

While FTSE Russell does not prescribe the number of disclosure channels a company must use, it places significant emphasis on Public Disclosure. In other words, sustainability information should be publicly available, easy to access, credible, verifiable, and presented consistently across all disclosure channels.

This means that achieving a strong ESG score is not simply about producing an excellent report. It is about ensuring that the same ESG information is disclosed strategically through the appropriate channels for different stakeholder groups.

One ESG Dataset, Four Disclosure Channels

In practice, Thai listed companies should prepare a single ESG dataset that is suitable for disclosure across four key channels. Although the underlying information remains the same, each channel serves a different purpose and addresses a different audience.

56-1 One Report

Prepared in accordance with the requirements of the Thai Securities and Exchange Commission (SEC). It provides investors with an integrated view of the organisation, covering business performance, financial information, corporate governance, risk management, and sustainability. Rather than presenting ESG as a standalone topic, the One Report demonstrates how sustainability is embedded within the company’s strategy and long-term value creation.

ESG Report or Sustainability Report

Provides a more comprehensive account of the organisation’s sustainability performance. This report allows companies to communicate environmental, social and governance initiatives in greater depth, including long-term commitments, ESG targets, key performance indicators, historical performance trends, and case studies that demonstrate measurable outcomes.

ESG Data Platform

A centralised system used to collect, manage, analyse and report ESG information in a structured format. The platform supports disclosure requirements forregulators, global ESG assessment organisations, investors and other capital market participants. Rather than simply acting as a reporting tool, it enables organisations to maintain consistent, traceable and assessment-ready ESG data across multiple reporting frameworks.

ESG Website

Arguably one of the most important disclosure channels today. An ESG website should no longer function merely as a repository for downloadable PDF reports. Instead, it should serve as a dedicated ESG Information Hub, presenting sustainability strategies, governance structures, climate commitments, performance data, policies, reports, news updates and supporting documents in a clear and intuitive structure. Well-designed navigation and direct links to policies and evidence allow investors, assessors and other stakeholders to locate relevant information quickly and efficiently.

Although these four channels are built upon exactly the same ESG dataset, they serve different purposes and audiences. Organisations should therefore avoid simply duplicating the same content across every platform. Instead, information should be tailored appropriately for each disclosure channel while remaining accurate, consistent and fully aligned.

ESG Disclosure Is No Longer a Year-End Exercise

Another area that many organisations underestimate is the disclosure timeline.

ESG disclosure is no longer an activity that begins once the sustainability report is ready. Instead, it is a year-round process that requires careful planning and coordination.

January and February

Organisations should begin collecting ESG information across all business functions, reviewing data completeness, and preparing content for the 56-1 One Report, Sustainability Report and other disclosure channels. This early preparation also helps ensure that reports can be finalised and published according to the annual reporting schedule.

March and April

Companies should complete and validate information within the ESG Data Platform, ensuring that all data has been reviewed and approved by management before submission.

Early May

Organisations should publish ESG information on their corporate website and submit their application for the FTSE Russell ESG Scores assessment.

June and September

FTSE Russell conducts its assessment using publicly available information. Companies are then typically given an opportunity to review preliminary results and provide additional supporting evidence during September and October, before the final ESG Scores are announced in December.

Viewed as a whole, ESG disclosure is no longer a one-off reporting exercise. It is a continuous process that requires organisations to manage information systematically throughout the year.

Every Piece of ESG Information Deserves to Be Seen

Producing a high quality ESG Report remains an essential foundation. However, the real challenge today is no longer collecting data, it is ensuring that the right information is disclosed through the right channels, at the right time, and in a format that is easy to find, understand and verify.

Organisations that perform well are not necessarily those producing the longest reports, but those that manage their ESG Disclosure Strategy effectively. From data collection and evidence management to disclosure through the 56-1 One Report, ESG Report, ESG Data Platform, and ESG Website, every stage contributes to how investors and ESG assessors perceive an organisation’s sustainability performance.

Ultimately, effective disclosure is about making every ESG effort visible, credible and valuable.

Because in today’s capital market,

The Right Disclosure. Makes Every ESG Effort Count.

ESG Report 2026: No Longer Just a Report, But a Test of Readiness

ESG reporting for Thai listed companies is entering a major transition. What used to be seen as a sustainability disclosure exercise is now becoming a board-level agenda that reflects how well a company manages risk, governance, data quality, and long-term value creation.

With the adoption of ISSB Standards, including IFRS S1 and IFRS S2, ESG Reports will need to go beyond describing sustainability activities. Companies will be expected to explain how sustainability-related risks and opportunities affect their business, how these issues are governed, how risks are managed, and which metrics and targets are used to track performance.

This shift also connects directly with the increasing importance of FTSE Russell ESG Scores, investor expectations, climate-related disclosures, and the quality of information disclosed through the 56-1 One Report, Sustainability Report, and ESG Website.

What Is Changing in ESG Reporting?

Under IFRS S1, companies are required to disclose material sustainability-related financial information, including ESG risks and opportunities that may affect cash flows, access to capital, and enterprise value.

IFRS S2 focuses specifically on climate-related disclosures. This includes climate risks and opportunities, physical risks, transition risks, and greenhouse gas emissions across Scope 1, Scope 2, and Scope 3.

In Thailand, the first phase of implementation will follow a “climate-first” approach. This means companies should begin by strengthening climate-related data, greenhouse gas emissions data, governance structures, risk management processes, and disclosure controls.

In practice, a strong ESG Report will no longer be judged only by how well it is written. It will be judged by how credible, traceable, and decision-useful the information is.

Key Timeline for Thai Listed Companies

The implementation of the FTSE Russell indicators

2025 reporting year / 2026 report discloses

Sustainable and Responsible Investing Funds, or SRI Funds, will be required to disclose information under the new SRI Fund criteria. These requirements aim to enhance transparency, reduce greenwashing risks, and help investors compare sustainability performance more clearly.

2027 reporting year / 2028 report discloses

The requirements will begin to apply to companies in the SET50.

2028 reporting year / 2029 report discloses

The requirements will be expanded to companies in the SET100.

2029 reporting year / 2030 report discloses

The requirements will apply to all listed companies on the Stock Exchange of Thailand, including companies preparing for IPOs.

2030 reporting year / 2031 report discloses

The requirements will apply to companies listed on the Market for Alternative Investment, or mai, as well as REITs, Infrastructure Trusts, Property Funds, and Infrastructure Funds.

This timeline gives companies time to prepare, but it should not create a false sense of comfort. ESG data, especially climate-related data and greenhouse gas emissions data, cannot be built properly at the end of the reporting year. Companies need systems, data owners, internal controls, and evidence trails in place early.

Three ESG Reporting Priorities Companies Should Start Now

1. Prepare Climate-related Disclosures

Companies should begin preparing information on climate-related risks and opportunities, including Scope 1 and Scope 2 greenhouse gas emissions.

Scope 1 covers direct emissions from company-controlled sources. Scope 2 covers indirect emissions from purchased energy. These data points require reliable calculation methods, clear data sources, supporting evidence, and, in many cases, readiness for external verification.

2. Manage ESG Data Across the Value Chain

Although early implementation in Thailand will focus mainly on Scope 1 and Scope 2 emissions, companies should also start preparing for Scope 3 disclosure.

Scope 3 covers greenhouse gas emissions across the value chain, including upstream and downstream activities. This may involve suppliers, contractors, logistics providers, distributors, and product use by customers.

The challenge is that much of this information does not sit within the company. Companies should therefore begin engaging key suppliers, mapping value chain data, and building practical data collection processes as early as possible.

3. Strengthen Sustainability Governance and Risk Management

Under the new ESG reporting requirements, companies must clearly disclose how sustainability and climate-related issues are governed.

This includes the roles of the board, executives, committees, and working teams. Companies must also show how ESG risks are assessed, managed, and connected to business strategy.

IFRS S1 and IFRS S2 follow four core disclosure pillars:

Governance

Strategy

Risk Management

Metrics & Targets

This means ESG reporting is no longer the sole responsibility of the Sustainability team. It requires collaboration across risk management, finance, accounting, operations, procurement, human resources, legal, marketing, and the board of directors.

What Companies Should Do Today

To prepare for ESG Report 2026 and upcoming ISSB-based disclosure requirements, companies should begin with the following actions:

Map new ESG reporting requirements against existing internal data.

Assign clear data owners for each ESG and climate-related data point.

Organise Scope 1 and Scope 2 greenhouse gas emissions data for verification.

Start planning Scope 3 data collection with key suppliers and business partners.

Connect ESG issues with enterprise risk management and business strategy.

Align disclosure content across the 56-1 One Report, Sustainability Report, ESG Website, and FTSE Russell ESG Score requirements.

Build internal readiness among the people responsible for ESG data, governance, and disclosure.

From Compliance to Business Readiness

The new ESG reporting requirements may appear to be another compliance burden. However, they also create an important opportunity for companies to strengthen risk management, improve data quality, build investor confidence, and prepare for future expectations from regulators, capital markets, and global sustainability standards.

A strong ESG Report is no longer just a communication document. It is evidence of business readiness.

For Thai listed companies, ESG reporting in 2026 and beyond will be about more than disclosure. It will be about whether the organisation has the governance, systems, data, and accountability needed to manage sustainability risks and opportunities in a credible and future-ready way.

References

Stock Exchange of Thailand, summary of Thailand’s sustainability disclosure requirements in alignment with ISSB Standards, including the phased implementation timeline for SET50, SET100, SET-listed companies, mai-listed companies, trusts, and related funds. https://setsustainability.com/page/disclosure

Securities and Exchange Commission, Thailand, announcement on revised SRI Fund disclosure criteria to strengthen transparency, reduce greenwashing risks, and improve sustainability-related fund disclosure. https://www.sec.or.th/TH/Pages/News_Detail.aspx?SECID=12343

Working on ESG All Year But Still Not Getting the FTSE Russell Score You Deserve?

Let’s Fix That: Build a Simple Data System That Actually Gets You Points

Your ESG Score Didn’t Meet Your Goal—Even Though You Did the Work

You’ve been running ESG programs all year. You have sustainability policies in place. But your FTSE Russell ESG score still isn’t where you want it to be. Sound familiar? Here’s the good news: you’re probably doing more than you think. The issue isn’t the work itself—it’s how you’re organizing and showing that work. This year, let’s change that by setting up a straightforward data system that helps evaluators see what you’re actually doing.

Introduction

Many organizations have received their FTSE Russell ESG Rating scores, which were released in December 2025. Congratulations to those who achieved their target scores. For organizations that fell short, you might feel disappointed and wonder, “Why didn’t our score improve as expected when we’ve implemented so many ESG initiatives?” The answer isn’t about doing too much or too little work—it’s about having systematic data collection, documentation and evidence management, and disclosure practices that allow assessors to properly evaluate and score your efforts. This article provides an actionable roadmap to help you establish an ESG data management system throughout the year, enabling you to systematically elevate your scores with principles that support long-term sustainable operations.

Understanding FTSE Russell ESG Rating Assessment Principles

FTSE Russell assesses ESG based on verifiable data and disclosures with a clear audit trail for data sources. Publicly listed companies are evaluated annually, with the assessment cycle typically running from June through March of the following year. Scores become available approximately four weeks after the Index Review in June, with official results announced in December.

A critical part of the process is the Company Review Period, when companies can provide additional information. This is an essential opportunity for companies to clarify data and address questions from FTSE Russell, which can result in higher scores. Here’s a summary of what you need to ensure to earn.

5 Main Reasons Your Score Isn’t Improving Despite Additional Work

Based on experience working with multiple organizations, here are five commonly encountered issues:

1. Scattered Data with No Clear Data Owner or Job Owner

ESG data often resides across different teams and files, using inconsistent definitions. When compiling data for reporting, this frequently leads to inconsistencies or overlapping data that’s difficult to explain and utilize effectively.

2. Evidence Isn’t Public or Can’t Be Found

Even when organizations genuinely implement initiatives, if evidence isn’t publicly disclosed or easily searchable, assessors cannot award points. This causes organizations to miss out on well-deserved scores.

3. Irregular Data Collection Cycles

The “compile everything at year-end” approach often results in missing critical data or misalignment with assessment cycles. Year-end data collection not only risks incomplete data but also creates significant headaches for the team.

4. Policies Without Measurement, Plans Without Results

Since FTSE Russell assesses both “structure” and “outcomes,” having only policies without KPIs, or only numbers without governance frameworks, leads assessors to view the data as lacking foundation, resulting in incomplete scoring.

5. No Quality Assurance/Quality Control (QA/QC)

Organizations that change policies, plans, and definitions every quarter show no continuity in their initiatives. When current year data can’t be compared with previous years, the credibility of the program diminishes.

Change your perspective and make your ESG program “scorable,” not just “doable.” The key principle to understand is that scores don’t come from good intentions but from “provable systems.” Therefore, establishing an effective ESG data management system is more important than conducting numerous ESG activities without systematic documentation.

Organizing ESG Data Collection in 5 Steps

If you don’t know where to start, try following these steps to establish a data management system and elevate your ESG reporting scores:

1. Analyze Scores and Gaps

Clearly identify “where points were lost” and “what should be improved first.” Review the latest assessment results broken down by Pillar (Environmental, Social, Governance) and prioritize data based on score concentration. This will reveal your “priority fix list” to identify what’s urgent and should be addressed first. Don’t forget to include the names of responsible parties, reviewers, and approvers for each topic to plan subsequent work.

2. Create an ESG Data Management System

Establish consistent data collection that allows year-round comparison. Develop a data framework that typically includes definitions for each indicator, collection methods, units of measurement, data collection scope, base year, and data sources. Develop tools or methods to track ESG work and data covering all indicators, data collection status, responsible parties, and supporting evidence or reference documents. Remember to align data collection cycles with annual assessment schedules.

3. Prepare Evidence and Reference Documents for Public Disclosure

Make evidence and reference data easily searchable, verifiable, and public. Create standardized datasets for organization-wide communication and collaboration, including policies, operational procedures, and KPI definitions, so the entire organization shares the same vision and moves toward common goals.

4. Design Disclosure Strategy

Ensure disclosed information is clear, relevant to the criteria, and matches FTSE Russell keywords. Structure your reports and ESG website pages for easy searching with clear categories and convenient access. Content should cover governance, policies and practices, goals and indicators, program progress, and verifiable reference evidence.

5. Test Run and Prepare for Assessment

Reduce risks before entering the actual assessment process. In this step, verify consistency between outcome figures, actual programs, disclosed reports, and reference documentation to ensure all data sets align. Assessors may have questions and follow-ups. At this juncture, readiness to respond quickly with supporting evidence is crucial to ensure your report doesn’t miss deserved points.

Quick Start Checklist

If you want to start immediately, here are 8 steps to take first:

Assign data owners for each ESG topic – Designate clear responsibility for each area (E, S, G)

Create a one-page summary showing where score gaps exist, starting with key indicators that most impact scores

Build an ESG data tracking sheet – Use Google Sheets or Excel, but it must be accessible to everyone

Create a folder for reference documents, supporting evidence, and related data with systematic structure for easy searching

Set clear data collection cycles – Monthly or quarterly depending on work nature and data type, add to calendar and notify all stakeholders

Summarize high-impact topics – Review the big picture and prioritize

Create an ESG Hub Page on your website – Even a simple page is better than nothing

Establish mandatory data review before any external submission or publication

Improve Your ESG Reporting Score with “Systems”, Not “More Work”

If your FTSE Russell ESG Rating score didn’t meet targets last year, this year is a golden opportunity to reset your approach. The critical shift is moving from year-end fire-drill ESG projects to creating a repeatable, continuous ESG management system that operates reliably year-round. When you have a solid system for data collection, evidence management, and disclosure, you’ll achieve:

Easier workflow for your team

Greater data credibility

Assessors able to score according to actual performance

More effective ESG communication for your organization

Are You Ready to Get Started?

If your organization needs additional consultation on establishing an ESG Data Management system or wants a customized FTSE Russell ESG Readiness Checklist designed specifically for your organization, don’t hesitate to contact us for further guidance.

5 key differences of SET ESG Ratings and FTSE Russell ESG Scores

Why FTSE Russell Matters for Thai Companies

ESG is no longer just about “responsibility”—it has evolved into an “investment standard” that drives global investor decision-making. The Stock Exchange of Thailand’s transition from SET ESG Ratings to FTSE Russell ESG Scores represents far more than a procedural change. It’s a pivotal shift that every listed company must understand and prepare for strategically.

FTSE Russell stands as a globally recognized ESG index and risk assessment provider, operating across over 80 countries worldwide and evaluating more than 85,000 companies throughout Europe, the Americas, and Asia. Its core strength lies in relying exclusively on publicly disclosed information, ensuring transparency, comparability, and verifiable assessment standards that meet international benchmarks.

To help Thai listed companies navigate this transition effectively and leverage this opportunity to elevate their organizational sustainability, this article examines the 5 fundamental differences between SET ESG Ratings and FTSE Russell ESG Scores. We’ll explore the transition roadmap you need to understand and provide systematic preparation strategies for your organization.

Figure 1FTSE Russell ESG Scores Model

The 5 key differences Thai ESG Ratings/Scores

1. Scoring Systems and Performance Disclosure

One of the most significant distinctions between SET ESG Ratings and FTSE Russell ESG Scores lies in their “scoring methodology” and “public disclosure” of results—a paradigm shift that fundamentally impacts corporate reputation, transparency, and investor confidence.

Under SET ESG Ratings, companies receive tier-based ratings (BBB, A, AA, or AAA) only when they meet minimum qualifying thresholds. Beyond achieving scores above 50% across each dimension (Environmental, Social, Governance), companies must satisfy additional requirements such as maintaining a CGR rating of at least 3 stars and demonstrating no negative governance issues during the assessment period. Companies failing to meet these criteria receive no public rating disclosure whatsoever.

FTSE Russell ESG Scores takes the opposite approach, implementing unconditional disclosure of all company scores using a decimal-based system ranging from 0.0 to 5.0. Regardless of performance level, all scores will be publicly announced starting in 2026, providing open access to investors and the general public.

While detailed insights such as thematic scores, dimensional breakdowns, or individual indicator performance remain accessible only within FTSE Russell’s proprietary system using company-specific access codes, the overall score—representing your organization’s “ESG identity” on the global stage—becomes universally visible. Whether you achieve a 4.8 or 0.9, the result is transparent to all stakeholders.

This transparency extends beyond mere openness to directly impact corporate “credibility.” Low scores without adequate explanation or appropriate disclosure may lead investors to conclude that the organization lacks genuine ESG commitment or systematic sustainability management practices.

This difference transcends scoring methodology—it represents a fundamental shift from “seeking assessment” to “communicating transparency” continuously through verifiable, publicly disclosed information.

In an era of heightened investor focus on ESG factors, companies that strategically manage their disclosure practices will not only achieve scores reflecting their true potential but also earn sustainable “stakeholder confidence.”

Summary

SET ESG Ratings

Scores only companies that “meet qualifying thresholds”

Announces results in tier format: BBB, A, AA, AAA

FTSE Russell ESG Scores

Scores all companies regardless of performance level

Uses decimal scoring format: 0.0–5.0

Publicly announces overall scores starting in 2026

Detailed insights (thematic scores, dimensions, indicators) accessible only through company-specific system access

The Advantage

FTSE Russell operates on principles of “transparency and equality”—every company has the opportunity to communicate ESG progress, not just those meeting minimum thresholds.

2. ESG Data Collection Methodology

Another game-changing distinction lies in the approach to ESG data collection. SET ESG Ratings requires companies to voluntarily register and complete comprehensive questionnaires with extensive supporting documentation from both public sources and internal records for Stock Exchange evaluation.

FTSE Russell ESG Scores eliminates questionnaires entirely, instead evaluating companies based solely on “publicly disclosed information”—sustainability reports, annual reports, Form 56-1 One Reports, and corporate websites. No internal documentation receives consideration.

This philosophy reflects international capital market principles emphasizing the ability to “communicate sustainability” directly, clearly, and accessibly. Companies capable of systematically disclosing ESG information can confidently navigate assessments without dedicating time and resources to hundreds of questionnaire responses.

Simultaneously, this signals that ESG disclosure should not be limited to assessment seasons but should represent “continuous public transparency”—robust, evidence-backed, and consistently verifiable information.

Summary

SET ESG Ratings

Companies must register and complete assessment forms

Requires internal documentation such as undisclosed policies and reports

FTSE Russell ESG Scores

No registration or form completion required—all listed companies assessed automatically

Uses exclusively publicly disclosed information:

Sustainability Reports

Annual Reports

Form 56-1 One Reports

Official corporate websites

The Advantage

Companies avoid duplicative work while establishing “comprehensive disclosure systems” that are accurate, complete, and easily accessible—benefiting investors and all stakeholders alike.

3. Review Process and Supplementary Information

FTSE Russell recognizes that assessments based solely on public disclosure may contain gaps, therefore designing a process enabling companies to review and provide additional information before final results are announced. Companies receive email notifications from FTSE4GOOD approximately September through October each year to access the FTSE Russell Platform and review their preliminary results.

Within this system, companies can provide commentary, submit additional reference documents, or clarify information not yet reflected in public sources. Organizations have approximately one full month to complete this process—a critically important window of opportunity. Once the deadline passes, FTSE Russell closes the system, accepts no additional information, and proceeds to finalize scores officially, announcing results in December of the same year.

This period represents a golden opportunity for companies to provide context, supplement missing information, or correct misunderstandings before final scores are transparently published to global investors and stakeholders. Importantly, these scores remain unchanged until the following year’s assessment cycle.

Companies missing this window—whether due to outdated contact information preventing notification receipt or lack of system response—must accept scores based solely on available information. In cases of low scores, this can immediately impact reputation and investor confidence on the international stage.

FTSE Russell provides companies the opportunity to

Review preliminary results and provide feedback within the system

Timeframe: September–October annually

Duration: Approximately one month

Method: Email notifications sent to designated company contacts

Companies can use this period to:

Verify information accuracy

Provide supplementary information or correct discrepancies

Update contact details to avoid missing notifications

Upon deadline expiration, FTSE Russell finalizes and announces scores in December.

4. Business Grouping and Industry Classification Systems

An accurate ESG assessment cannot apply uniform criteria across all businesses, as risks and material issues vary distinctly by industry. Business classification represents another critical difference between SET ESG Ratings and FTSE Russell ESG Scores.

Business Grouping and Industry Classification of SET ESG Ratings

It employs the Stock Exchange of Thailand’s classification structure, dividing companies into 8 major industry groups:

Agribusiness & Food

Consumer Products

Financials

Industrials

Property & Construction

Resources

Services

Technology

Each group subdivides into 28 business sectors for assessment and comparison of similar companies—such as banking, energy, food & beverage, communications, etc. While suitable for Thai capital market management, this system has limitations in granularity and alignment with global ESG standards. Despite effectively reflecting the Thai market overview, it cannot achieve the depth of segmentation or international benchmarking required for sophisticated analysis.

Business Grouping and Industry Classification of FTSE Russell ESG Scores

It utilizes the ICB (Industry Classification Benchmark)—a globally recognized industry classification system used by investors and stock exchanges across over 80 countries, enabling accurate and fair cross-sector, cross-border company comparisons.

ICB divides industries into 11 primary groups:

Oil, Gas and Coal – Traditional energy businesses including oil, natural gas, coal

Basic Materials – Raw materials and mining including metals, chemicals, plastics, paper

Industrials – Machinery, heavy industry, engineering, general manufacturing

Consumer Discretionary – Non-essential goods and services including automotive, apparel, furniture, entertainment

Financials – Banking, insurance, funds, and various financial services

Real Estate – Property development, asset management for residential, commercial, or industrial properties

Technology – Software, hardware, electronics, telecommunications, IT services

Telecommunications – Telephone networks, internet, satellite, and other communication services

Utilities – Public utilities including electricity, water, gas, and renewable energy

ICB extends beyond primary industry groups, subdividing into 20 Supersectors, 45 Sectors, and ultimately 173 Subsectors at the most granular level. This enables FTSE Russell assessments to identify ESG issues material to each specific business type with precision.

For example, a property development company operating in Thailand might be classified under “Real Estate Development,” which has entirely different indicators from “Real Estate Investment Trusts (REITs)” or “Construction & Engineering,” despite all falling under the broader real estate category.

Furthermore, FTSE Russell considers the operational country context. Companies based in developing countries may need greater emphasis on human rights or anti-corruption measures rather than carbon issues in certain cases. The system analyzes “materiality levels” for each ESG theme, then weights indicators appropriately for that specific business. This represents “Context-Based ESG Scoring”—emerging as the new global standard.

Summary

SET ESG Ratings

Uses Thai Stock Exchange criteria

Divides into 8 industry groups / 28 business sectors

FTSE Russell ESG Scores

Uses ICB – Industry Classification Benchmark

International standard used across 80+ countries

Divides into 11 primary industry groups with detailed segmentation to 173 subsectors

Considers “primary revenue sources” identified in financial statements and One Reports

Multi-business companies may span multiple subsectors

Considers “operational country context” concurrently

Strength

FTSE Russell assesses based on “actual business risks” and country context, delivering accurate and internationally relevant ESG profiles.

5. Indicator Quantity and Complexity Levels

While both SET ESG Ratings and FTSE Russell ESG Scores measure from similar core dimensions—Environmental (E), Social (S), and Governance (G)—the clear distinction lies in the depth, specificity, and structural design of FTSE Russell’s indicator framework.

SET ESG Ratings employs approximately 140-150 indicators, predominantly general metrics applied universally across all industries, with only minimal adjustments for specific business characteristics.

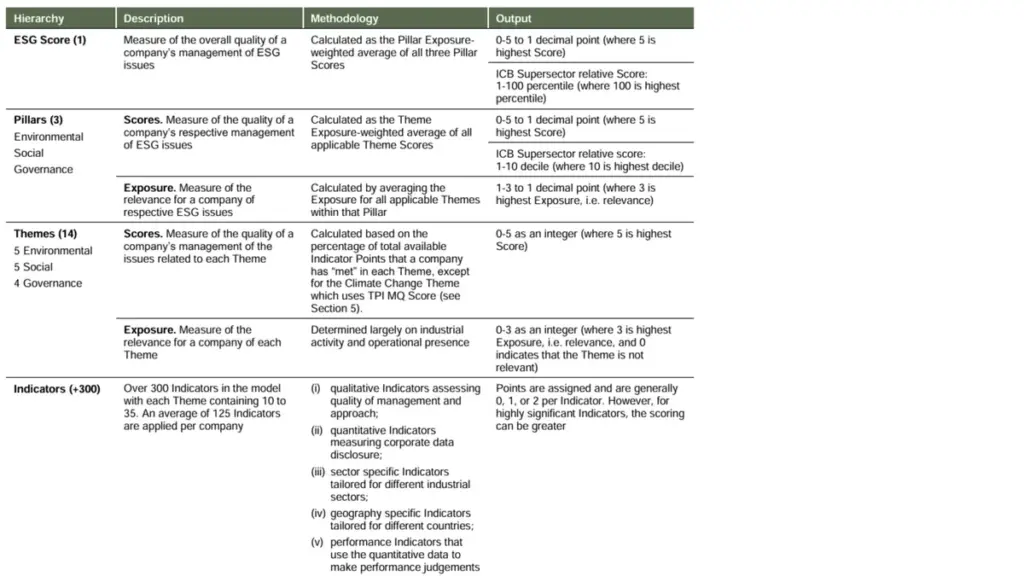

FTSE Russell ESG Scores utilizes a more comprehensive and flexible indicator set, comprising over 300 indicators divided into two categories:

Universal indicators representing approximately 56%

Sector- and Country-specific indicators comprise the remaining 44%, which vary according to industry characteristics and the operational context of each country.

Each company is not assessed against all 300+ indicators simultaneously, but rather evaluated on what is “genuinely material,” averaging approximately 125 indicators per company. This reduces reporting burden while enabling scores to more precisely reflect organizational capabilities.

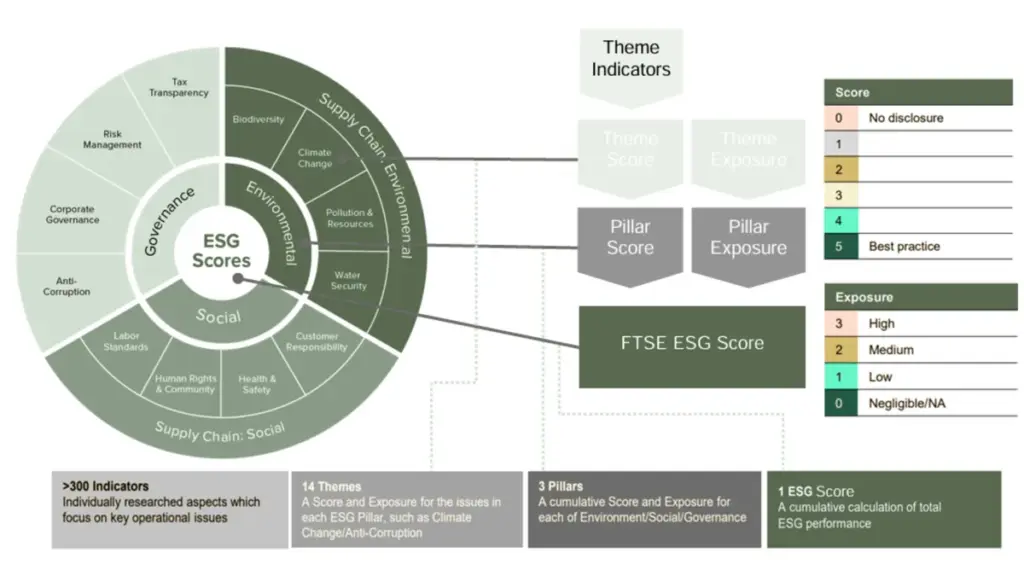

All FTSE Russell ESG Scores indicators are categorized under 14 ESG Themes linked to systematic global ESG risks, organized across three core dimensions:

Environmental

Biodiversity

Climate Change

Pollution and Resources

Water Security

Supply Chain (Environment)

Social

6. Human Rights and Community

7. Labor Standards

8. Health and Safety

9. Customer Responsibility

Governance

10. Risk Management

11. Tax Transparency

12. Anti-Corruption

13. Corporate Governance

14. Supply Chain (Social)

The distinctive feature of FTSE Russell’s system lies in risk materiality assessment for each theme across industries, categorized into four levels:

High (Very high risk)

Medium (Moderate risk)

Low (Low risk)

Not Relevant (Not applicable)

When any theme receives a “Not Relevant” (N/A) assessment for a specific business, the company will not be evaluated on that theme, and it will have zero impact on overall ESG score calculations.

For example, if a company operates in digital services, “Water Security” might be classified as Not Relevant due to minimal water usage in operations. Conversely, for mining or agricultural businesses, this theme might receive a High classification, requiring serious management and disclosure commitments.

Additionally, certain indicators maintain heightened intensity requirements, such as three-year historical data disclosure, external verification, or demonstrable impact measurement rather than mere policy statements or commitments.

This comprehensive approach means FTSE Russell ESG Scores evaluate not just “what organizations have” but rather “how organizations manage risk and create transparency” in matters most material to their specific context.

Summary

SET ESG Ratings

Approximately 140-150 indicators

Predominantly general metrics

FTSE Russell ESG Scores

Over 300 indicators

Divided into:

56% universal indicators

44% specific indicators (industry + country-specific)

Certain indicators maintain high intensity requirements:

Three-year historical data disclosure

External verification requirements

Recommendation

Companies should systematically study FTSE indicators to strategically plan comprehensive disclosure aligned with their specific context.

Figure 2FTSE Russell ESG Scores Data structure

Timeline for FTSE Russell ESG Scores Transition

Year

Development

2024

Leading listed companies begin pilot FTSE Russell assessments

2025

Companies may “voluntarily” request assessments

2026

FTSE Russell ESG Scores fully operational, officially replacing SET ESG Ratings

Preparation Strategies for FTSE Russell ESG Scores

1. Develop Transparent ESG Data Architecture

As Thailand’s ESG assessment system transitions from questionnaire-based evaluation to comprehensive public disclosure assessment, companies preparing for FTSE Russell ESG Scores must establish not only clear ESG policies but also “disclosure systems” that are transparent, systematic, and accessible beyond previous requirements.

Preparation extends beyond content to encompass processes, mindset, and continuity of information that organizations choose to communicate publicly through published documents, website-hosted reports, and internal systems supporting consistent disclosure practices.

2. Enhance Website Disclosure Systems

Corporate websites, typically the first point of reference, require structured ESG or IR (Investor Relations) menu organization with current information and comprehensive linkage to critical documents such as Sustainability Reports, ESG Policies, GHG Emissions data, and organizational values. This prevents assessor confusion or misinterpretation from fragmented information.

3. Verify Three-Year Historical Data

FTSE Russell considers three-year historical data across multiple indicators, particularly for trend analysis such as carbon reduction or female executive representation. Companies should ensure quantitative evidence (KPIs and performance data) is maintained consistently and consider external verification (auditor or verifier certification) for certain data points to enhance disclosure credibility.

4. Update Company Contact Information

This seemingly minor detail often causes organizations to miss critical opportunities, especially approaching annual assessment periods. Organizations not receiving FTSE4GOOD email notifications during September-October will forfeit opportunities to review preliminary results or submit additional system information, potentially resulting in December score announcements that fail to reflect current company data.

The Transition as Strategic Opportunity (Not to Be Overlooked)

FTSE Russell ESG Scores represents more than a “new assessment system”—it’s a powerful opportunity to elevate Thai organizations’ internal management capabilities and genuinely open doors to the global ESG stage.

Many perceive ESG disclosure as burdensome—filled with reports, indicator tables, and management obligations. In reality, organizations beginning with proper system establishment from the outset discover it’s not only manageable but becomes a process enabling profound organizational self-examination in previously unconsidered dimensions.

Data previously scattered across departments, explanations once limited to “internal use,” and problems whose “root causes remained unknown” gradually emerge clearly as you systematize, create disclosure frameworks, and communicate authentically.

This represents an organizational “transformation” period—not for assessment compliance but for identifying inefficiencies, financial leakages, or hidden risks, and areas deserving reinforcement because they create long-term business and sustainability value.

Early-adopting companies gain advantages beyond scoring—they achieve “self-awareness and understanding.” When you know your global positioning, you advance with greater confidence than others.

In the ESG landscape, transparency isn’t a burden but a tool for building credibility and strategic advantage, plus organizational self-understanding—all beginning with strategic and intentional “disclosure.”

A guide to understanding the FTSE Russell ESG Scores for corporate leaders

What is FTSE Russell ESG Scores

FTSE Russell is a framework designed for worldwide companies to evaluate their performances in three pillars; Environmental, Social, and Governance. In collaboration with the Stock Exchange of Thailand (SET) and the London Stock Exchange Group (LSEG) launched a comprehensive assessment framework for benchmarking, analytics, and data solutions for investors. The purpose of this framework is increasingly significant for publicly listed companies as investors progressively incorporate sustainability factors into their investment decisions.

The Explanation of FTSE Russell ESG Scores

The FTSE Russell ESG Rating methodology assesses companies across 14 ESG themes containing over 300 individual indicators. They are divided into (1) general indicators and (2) industry group indicators, with each listed company being assessed on average around 125 indicators, with the FTSE Russell indicators giving approximately 56% weight to general questions and 44% to questions that delve deeper into sectors and countries.

These themes are categorized into three pillars: Environmental, Social, and Governance.

The Environmental pillar examines how companies manage their impact on the natural world, focusing on climate change strategies, water security measures, biodiversity protection efforts, and pollution control systems. Companies are evaluated on their policies, programs, targets, and actual performance in reducing their environmental footprint.

The Social pillar assesses how organizations interact with employees, customers, suppliers, and their communities. This includes labor standards and working conditions, human rights policies and community engagement, health and safety protocols, and customer responsibility practices such as product safety and data protection.

In the Governance pillar, FTSE Russell examines corporate structures and processes that ensure proper oversight, accountability, and ethical business conduct. Key areas include board composition and effectiveness, anti-corruption measures, tax transparency, and comprehensive risk management frameworks.

Companies are evaluated on both their exposure to ESG risks (determined by their industry and geographic operations) and the quality of their management response to these risks. This creates a balanced assessment that recognizes both inherent operational challenges and management effectiveness. For example, an oil company may have high environmental risk exposure but could still score well if it demonstrates exceptional management of those risks relative to industry peers.

SET ESG Rating vs. FTSE Russell ESG Scores: Key Differences

The Stock Exchange of Thailand (SET) ESG rating system and FTSE Russell’s framework share similar objectives but differ in several important aspects.

In terms of geographic focus, SET ESG is explicitly designed for the Thai market and business environment, whereas FTSE Russell applies global standards that enable international comparability. This distinction is crucial for companies with international investors or ambitions for global expansion.

The methodology also differs significantly. SET ESG is tailored to the Thai business context, taking into account local regulatory requirements and market conditions. FTSE Russell employs a standardized global methodology that allows for cross-border and cross-industry comparisons, making it particularly valuable for international investment decisions.

The assessment process varies as well. SET ESG typically conducts annual assessments based primarily on company disclosures. FTSE Russell employs continuous assessment with more frequent updates, incorporating a wider range of data sources beyond company reports. This provides a more dynamic and comprehensive view of a company’s ESG performance.

Data sourcing represents another key difference. While SET ESG relies predominantly on company-disclosed information, FTSE Russell supplements this with multiple sources including third-party data, news analysis, and stakeholder reports. This multi-source approach helps validate company claims and provides a more objective assessment.

Thematic coverage also distinguishes the two frameworks. SET ESG focuses on issues particularly relevant to the Thai market and regulatory environment. FTSE Russell covers a comprehensive range of global ESG issues, which may include emerging risks that are not yet prevalent in Thailand but are important to international investors.

Finally, the scoring systems differ in presentation. SET ESG uses a stars-based rating system (1-5 stars), while FTSE Russell employs a numerical scale ranging from 0.0 to 5.0, wherein a score of 0.0 indicates an absence of evaluative information, and a score of 5.0 represents the pinnacle of best practices. The FTSE Russell approach allows for more granular differentiation between companies and clearer tracking of incremental improvements.

The key distinction is that while SET ESG provides valuable insights into the Thai market, FTSE Russell offers a globally recognized benchmark that enables international comparisons and attracts a broader range of global investors.

Opportunities for High-Scoring Companies

Companies that achieve high scores in the FTSE Russell ESG Scores can leverage several significant advantages in today’s sustainability-focused business environment.

Enhanced access to capital represents perhaps the most tangible benefit.

Global investment firms managing trillions in assets use FTSE Russell ESG ratings to screen potential investments. High-scoring companies gain privileged access to ESG-focused investment funds, which have seen record inflows in recent years. They may also secure green bonds and sustainability-linked loans at favorable rates, reducing capital costs. Furthermore, they attract long-term institutional investors who value sustainability as a proxy for management quality and future resilience.

Strong ESG performance also offers substantial competitive differentiation. Companies with high FTSE Russell ratings enjoy improved reputations among stakeholders, which translates into enhanced brand value and customer loyalty, particularly among younger consumers who increasingly make purchasing decisions based on sustainability criteria. This reputation advantage extends to stronger positioning in competitive tenders, particularly for government and corporate contracts that increasingly incorporate ESG requirements.

Risk mitigation and operational efficiency present another valuable opportunity.

The framework encourages risk management practices that lead to reduced exposure to environmental and social risks, which can manifest as costly disruptions, litigation, or regulatory penalties. Companies often experience lower compliance costs through proactive management rather than reactive responses to new requirements. Many sustainability initiatives simultaneously enhance operational efficiency through resource optimization, whether in energy, water, or materials. Additionally, strong ESG performers face a reduced likelihood of regulatory penalties as they typically exceed compliance requirements.

Global recognition and stakeholder trust

High FTSE Russell ratings provide international recognition of sustainability leadership that extends beyond national borders which investors can compare scores with listed companies around the world. This improved credibility with multinational partners and customers who increasingly screen their supply chains for sustainability risks. Strong performers also develop stronger relationships with regulators and policymakers, potentially influencing future policy development. The reputation benefits extend internally as well, enhancing employee and talent attraction and retention in competitive talent markets where purpose-driven organizations have advantages.

Practical Implementation for Thai Companies

For Thai corporate leaders looking to improve their FTSE Russell ESG performance, several strategic approaches can yield significant results.

You better start with gap analysis and strategy development, which represent essential first steps. Companies should comprehensively compare their current sustainability practices against FTSE Russell metrics to identify strengths and weaknesses. This assessment helps identify high-impact improvement areas based on materiality assessment—focusing resources where they will have the greatest effect on both sustainability outcomes and ratings improvement. With this understanding, organizations can develop a comprehensive ESG strategy with clear goals, timelines, and accountability measures that align with both business objectives and FTSE Russell criteria.

Governance structure enhancement often yields substantial rating improvements. This involves ensuring board-level oversight of ESG matters, with clear reporting lines and regular sustainability discussions at the highest organizational level. Companies should establish clear accountability for sustainability performance through designated roles and compensation links. Integrating ESG considerations into risk management frameworks helps identify emerging issues before they become problems and demonstrates a sophisticated management approach to potential investors.

Robust data management and disclosure systems are increasingly critical. Leading companies implement specialized systems to collect, verify, and report ESG data with the same rigor as financial information. Aligning disclosures with international standards such as GRI, SASB, and TCFD ensures compatibility with investor expectations and rating methodologies. Transparency in both successes and challenges builds credibility with raters and investors, who recognize that sustainability transformation is a journey rather than an immediate destination.

Stakeholder engagement complements these technical approaches. Companies should regularly engage with investors to understand their evolving ESG expectations and priorities. Collaboration with industry peers on common sustainability challenges can accelerate progress and demonstrate sector leadership. Participation in relevant sustainability initiatives and platforms increases visibility and provides valuable learning opportunities that can inform internal practices.

In the era of responsibility

The FTSE Russell ESG framework represents more than just a rating system—it offers a roadmap for sustainable business transformation. For Thai corporate leaders, understanding and implementing this framework can drive long-term value creation while meeting the growing expectations of global investors and stakeholders.

By strategically approaching the FTSE Russell assessment, companies can transform sustainability compliance into a competitive advantage, accessing new capital opportunities while building resilience for the future. In an era where sustainable business practices increasingly define market leaders, high FTSE Russell ratings serve as both validation of current excellence and a foundation for continued success in an evolving business landscape.

the Most Renowned ESG Voluntary Frameworks: Dow Jones Sustainability Indices (DJSI)

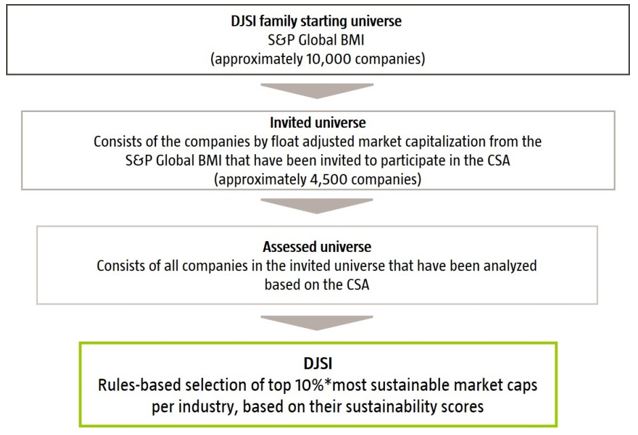

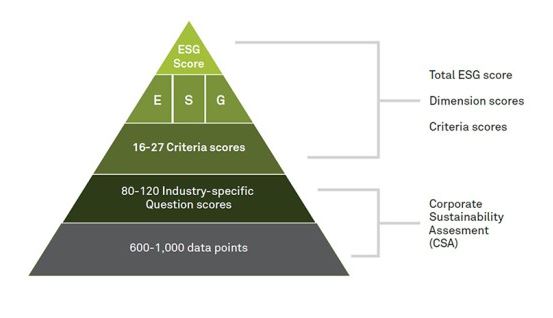

The Dow Jones Sustainability Indices (DJSI) are a family of best-in-class benchmarks for investors who have recognized that sustainable business practices are critical to generating long-term shareholder value and who wish to reflect their sustainability convictions in their investment portfolios. The family was launched in 1999 as the first global sustainability benchmark and tracks the stock performance of the world’s leading companies in terms of economic, environmental and social criteria. Created jointly by S&P Dow Jones Indices and Robeco Sustainable Asset Management (SAM), the DJSI combine the experience of an established index provider with the expertise of a specialist in Sustainable Investing to select the most sustainable companies from across 61 industries. The DJSI World applies a transparent, rules-based component selection process based on the companies’ Total Sustainability Scores resulting from the annual S&P Global Corporate Sustainability Assessment (CSA). Only the top ranked companies within each industry are selected for inclusion in the Dow Jones Sustainability Index family. No industries are excluded from this process as shown in Figure 1.

* Global Indices: Top 10%, Regional Indices: Top 20%, Country Indices: Top 30%

Figure 1

The composition of the DJSI is reviewed each year in September based on the S&P Global ESG Scores resulting from the annual SAM and CSA and is rebalanced quarterly (S&P Global, 1, 2023). The CSA has become the basis for numerous ESG indices over the last two decades. S&P Global acquired the CSA in 2019, which included the transition of the related ESG ratings and ESG benchmarking teams and that now operate out of S&P Global Switzerland. The Corporate Sustainability Assessment (CSA) empowers you to leverage the unique expertise and the proprietary methodology and database underlying the world’s most renowned sustainability indices (S&P Global, 2, 2023). While increasing numbers of companies have chosen to participate in the CSA, annual reviews have enabled the questions to be refined and streamlined over the years. The result is that currently relevant sustainability themes are combined with the systematic introduction of emerging sustainability issues and it can be said that it is the continuing evolution process of the CSA (S&P Global, 3, 2023).Starting April 2019, S&P DJI has begun further leveraging SAM sustainability data to deliver an extensive range of ESG indices. The S&P ESG Index Family, which are sets of indices, offers investors exposure to companies according to their ESG profile in the context of country-specific and regional indices. The index families are based on S&P DJI ESG Scores, based on the results of the annual S&P Global Corporate Sustainability Assessment (CSA). The index family includes broad market indices like the S&P 500 ESG, S&P Europe 350 ESG, S&P Global 1200 ESG, and S&P Japan 500 ESG, designed to closely track their parent indices with similar risk and return profile and low tracking error. The key criteria for constituent eligibility and selection in the S&P ESG Index Family are the S&P DJI ESG Scores. The scores contain a total company-level ESG score for a financial year, comprising individual environmental (E), social (S), and economic & governance (G) dimension scores. The criteria scores are weighted to eliminate biases among different industries and companies that complete the CSA versus companies that are assessed on the basis of publicly available information. The methodology of the S&P ESG Index Family is constructed to be simple, with a selection process meant to keep index’s industry weights in line with S&P broad market indices. The index methodology results in improved composite ESG scores, and offers improved ESG performance across each industry group (S&P Global, 4, 2023). Figure 2 Shows the score of CSA and ESG Indices, and figure 3 shows an example feature of S&P ESG Indices (S&P Global, 5, 2023).

Figure 2

Figure 3

CSA Methodology

The Corporate Sustainability Assessment (CSA) will ask invited companies about methodologies and rationales of reporting in order to gather information from invited companies for calculating the S&P Global ESG Score, which is a crucial part of the Dow Jones Sustainability Indices (DJSI). CSA provides a guideline, called CSA Handbook, to be a check list for invited companies’ activities. For each covered question, this document provides the Assessment Focus, the Question Rationale, details of the Question Layout and specific guidance on how to answer. Moreover, the Question-Specific Guidance & Definitions sections define the terms that use and provide details on how to interpret and answer each question. They also specify the question’s alignment with the GRI or other standards and framework (Based on GRI mainly), and whether internal or public documents will be necessary to answer the question. The CSA is a holistic assessment, but the structure and weighting of each criterion depends on its financial materiality in a given industry. To aid companies’ preparation for the CSA, it shares the weights for the different aspects of the assessment under CSA Methodology. It also provides general guidance on how to complete the CSA, its expectations and some general tips for a successful submission. Each question in the questionnaire consists of one or more sub-questions. Invited companies are given the possibility of selecting one or more answers to each question. Each question also contains a standard set of answer options that enable you to indicate if a company do not have the information asked for or if the question is not applicable to that company. For the Assessment focus, there are icons to give an indication of what CSA looking for as showed in Figure 4 (S&P Global, 6, 2023).

Figure 4

Invited Companies

Every year more companies see the value of disclosing their sustainability performance to capital markets via active participation in the Corporate Sustainability Assessment (CSA). In 2023, 13,800 companies were invited to complete the CSA. Of those, 3,519 companies were eligible for selection into a Dow Jones Sustainability Index (DJSI). A record number of 1,728 DJSI eligible companies actively participated, an increase of 9% over last year in this group. Of all invited companies, 2,480 have already submitted, representing over 48% of global market capitalization, relative to the S&P Global Broad Market Index (BMI), up from 45% in 2021. The assessment is still ongoing until end of January. Participating companies can choose the degree to which they permit S&P Global to share underlying datapoints submitted in the CSA that are supplemental to the company’s public reporting. The majority of participating companies took advantage of this option to leverage S&P Global’s platforms to communicate this information to a wider capital market audience. To inform the growing number of ESG-focused investors about corporate sustainability performance. Companies will be invited in 3 groups, starting with those eligible for any Dow Jones Sustainability Index (DJSI), then companies will be chosen from 3 factors including:

All companies that participated in the CSA in previous year.

Companies invited as part of the eligible universe of the Dow Jones Sustainability Indices (DJSI), as well as numerous other S&P ESG indices.

Companies whose sustainability performance is considered to be of interest to the broader investment community.

Companies that are invited but decide not to participate may be assessed by S&P Global based on publicly available information, and the resulting ESG Scores and data may be shared via S&P Global platforms. Participation in the CSA is not a prerequisite for eligibility in the DJSI or other S&P ESG Indices. Official invitations will be sent out between February and June. Companies may also check their invitation status via CSA online platform.

Participation without invitation

Any company interested in the CSA that agrees to make their resulting ESG Score public on S&P Global platforms will be assessed free of charge by contact [email protected] for more information. The 2023 CSA questionnaire opens for all companies on April 4th. New for this year, companies are able to select an assessment window that best meets individual reporting schedules. Log in to the CSA Portal to reserve a slot (S&P Global, 7, 2023).

In Thailand, there are currently 26 Thai companies in DJSI, which is the highest number in ASEAN, including ADVANC, AOT, BANPU, BDMS, BJC, BTS, CPALL, CPF, CPN, CRC, DELTA, EGCO, GPSC, HMPRO, IRPC, IVL, KBANK, MINT, PTT, PTTGC, SCB, SCC, SCGP, TOP, TRUE and TU. There are 11 Companies among These 26 companies, which has world class potential to be in DJSI World Family and achieve ESG Index Family (SET, 2022).

S&P Global, 3 (2023) The S&P Global Corporate Sustainability Assessment. [online] New York: S&P Global. Available from: https://www.spglobal.com/esg/csa/about/ [Access 27 July 2023].

the Most Renowned ESG Voluntary Frameworks: Global Real Estate Sustainability Benchmark (GRESB)

GRESB is the global ESG benchmark for financial markets, which is established in 2009 and composed of an independent foundation and a benefit corporation. The GRESB Foundation focuses on the development, approval and management of the GRESB Standards while GRESB BV performs ESG assessments and provides related services to GRESB Members. GRESB is a mission-driven and industry-led organization that provides actionable and transparent environmental, social and governance (ESG) data to financial markets. The 2022 real estate benchmark covers more than 1,800 property companies, real estate investment trusts (REITs), funds, and developers. In addition, GRESB coverage for infrastructure includes over 800 infrastructure funds and assets. Combined, GRESB represents USD 8.6 trillion in real asset value. More than 170 institutional investors use GRESB data to monitor their investments, engage with their managers, and make decisions that lead to a more sustainable real asset industry. Led by a Foundation Board composed of representatives from GRESB Members and Partners, the GRESB Foundation is the primary platform for GRESB to engage with the industry, owning and governing the standards upon which GRESB BV – a separate profit-for-purpose benefit corporation – performs its assessments. The GRESB Foundation, GRESB BV and GRESB Members work as one to deliver a shared vision of an investment community that plays a central role in creating a more sustainable world, one where society can meet the needs of the present without compromising the ability of future generations to meet theirs. As an independent standards-setting body, the GRESB Foundation works to develop, maintain, improve and publish GRESB Standards annually, in time for GRESB BV to perform its assessments.

Specifically, the GRESB Foundation:

Facilitates active industry engagement and consensus on the GRESB Standards

Ensures that the standards are feasible and can be practically implemented

Provides inclusive representation across GRESB Members and Partners

Ensures that the standards continually evolve to advance the foundation’s mission

The GRESB Standards are a set of guidelines to assess and benchmark ESG and related performance of real and other assets. The Standards include the questions, evidence and indicators to assess ESG performance, including the weighting of the indicators. On 14 September 2022, the GRESB Foundation Board approved all the recommended changes for the 2023 GRESB Standards. This is an important outcome of the new GRESB Standards Development Process, which puts the voice and priorities of GRESB members and partners at the forefront of the global ESG realm (GRESB 1, 2023).

Stakeholder Engagement

GRESB’s stakeholder engagement strategy is built on the AA1000 AccountAbility Stakeholder Engagement Standard (2015) and references the ISEAL Alliance Standard-setting Code of Good Practice, which defines how a sustainability standard should be developed, structured and improved over time. To ensure stakeholder engagement is embedded across the organization, GRESB have committed to the AccountAbility principles of inclusivity, materiality, responsiveness and impact. For GRESB, the stakeholder landscape is complex, with some stakeholder groups overlapping others in terms of roles and responsibilities:

Investors, both institutional investors (pension funds, insurance companies, sovereign wealth funds) and other investors (banks, family offices, endowments, etc.)

Real estate & infrastructure entities, including listed property companies, developers, REITs and private funds

Industry associations, such as APREA (Asia Pacific Real Estate Association), ANREV (Asian Association for Investors in Non-Listed Real Estate Vehicles) or ARES Management Corp

Institutions like development banks, central banks, governments, and inter-governmental organizations

ESG framework providers, from both NGOs and the private sector

Inter-governmental initiatives, such as those related to the United Nations

Investor initiatives

Green Building Councils

Certification or rating scheme providers

Consultants either organization or individual

Media and research organizations

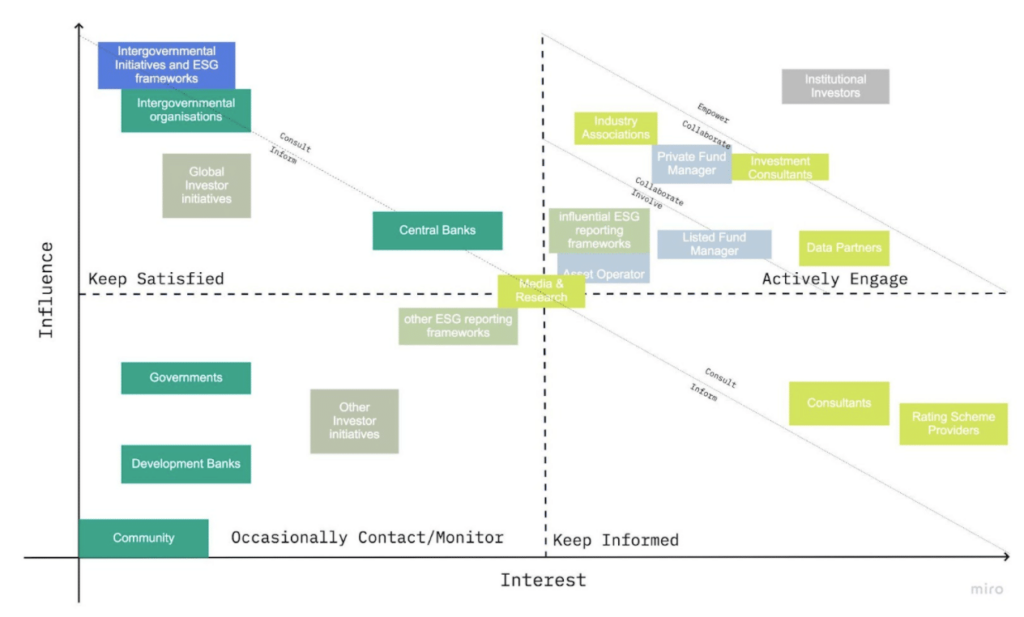

According to GRESB plays an important role within the world of sustainable real assets, and critically engage with the many stakeholders that operate in the ESG space. That said, they cannot and should not engage every stakeholder in the same way or at the same level. Therefore, an “interest-influence” grid helps illustrate our approach, which shows active engagement with GRESB Investor Members, Participant Members and Partners, which is done primarily through the GRESB Foundation as shown in Figure 1.

Figure 1

It can be seen that “influential ESG reporting frameworks” are among our most important stakeholders, just below our own members and partners. For these frameworks, we create bilateral partnerships and engage through representation on various committees and working groups such as Principles for Responsible Investment (PRI) The Global Reporting Initiative (GRI), The Sustainability Accounting Standards Board (SASB), The International <IR> Framework, EU Sustainable Finance Disclosure Regulation (SFDR), Task Force on Climate-related Financial Disclosures (TCFD), Carbon Disclosure Project (CDP) (GRESB 2, 2023). Especially, The EU’s Sustainable Finance Disclosure Regulation (SFDR) is a new transparency requirement for financial market participants related to key environmental, social and governance (ESG) criteria. The purpose is to increase market transparency and direct capital towards more sustainable businesses. SFDR imposes different disclosure obligations on Financial Market Participants, depending on their size and the nature of their products and/ or services. All participants in the EU will need to make general disclosures about sustainability practices for both the entity and their products and/ or services. They will also need to report on their Principle Adverse Impacts (PAIs), which are a series of indicators covering a range of ESG issues, such as greenhouse gas emissions and waste management. At the moment, most companies and funds do not provide disclosures or collect data that is granular enough to satisfy the requirement, once it goes fully in effect, or to provide investors with the level of transparency that is expected by this regulation. GRESB, hence, offers an assessment that provides Financial Market Participants with the framework they need for their Principal Adverse Impact Statement. The Assessment is comprised of around 60 ESG metrics that need to be reported on (GRESB 3, 2023). The SFDR Assessment consists of a number of aspects that a participant is required to report on, including:

Entity and Reporting Characteristics

Climate and other environment-related indicators

Social and employee, respect for human rights, anti-corruption and anti-bribery matters

The SFDR Assessment is broken into 3 parts to reflect the different tables of PAIs as outlined by the EU documentation. The Assessment evaluates performance against three ESG Components – Management, Performance, and Development. The methodology is consistent across different regions, investment vehicles and property types and aligns with international reporting frameworks, such as TCFD, GRI or PRI. The GRESB Real Estate Assessment provides investors with actionable information and tools to monitor and manage the ESG risks and opportunities of their investments, and to prepare for increasingly rigorous ESG obligations. These 3 tables are detailed as follows:

Table 1: Mandatory climate and other environment-related indicators, Social and employee, respect for human rights, anti-corruption and anti-bribery matters.

Table 1 focuses on 14 environmental and social indicators applicable to investments in investee companies and 2 indicators applicable to investments in real estate assets that have to be disclosed by financial market participants, these are considered as part of the “mandatory indicators that have to be reported on”.

Table 1 consists of 16 indicators across 7 aspects:

Greenhouse gas emissions

Biodiversity

Water

Waste

Social and employee matters

Fossil fuels (Real Estate specific indicators)

Energy efficiency (Real Estate specific indicators)

Table 2: Additional climate and other environment-related indicators. These are considered to be optional although participants are encouraged to report on at least one of those indicators in order to abide by regulatory requirements. Table 2 consists of 16 applicable to investment in investee companies and 5 indicators specific to real estate across 9 aspects:

Emissions

Energy performance

Water, waste and material emissions

Green securities

Greenhouse gas emissions (Real Estate specific indicators)

Energy consumption (Real Estate specific indicators)

Waste (Real Estate specific indicators)

Resource consumption (Real Estate specific indicators)

Biodiversity (Real Estate specific indicators)